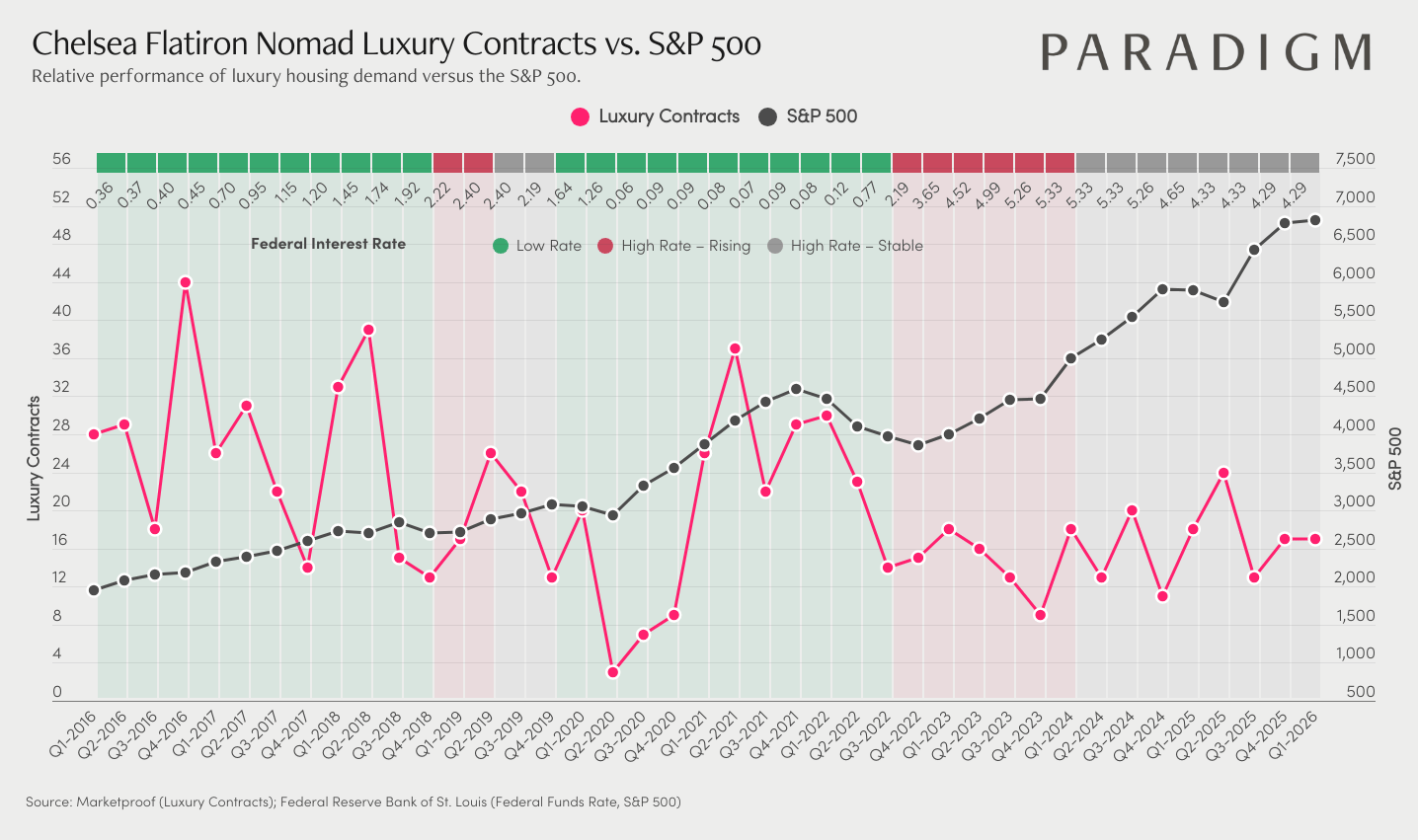

The Chelsea, Flatiron, and NoMad corridor is one of the more interesting stories among the neighborhoods we track. $4M+ contract volume hit 43 in Q4 2016 and climbed back to 36 during the 2021 rebound, showing that luxury buyer demand here can turn on quickly when conditions align.

What makes this corridor worth paying attention to right now is how wide the gap has gotten between equity market performance and local luxury activity. Contract volume has been running between 8 and 20 for most of the past two years, while the S&P 500 has pushed from around 4,000 to nearly 6,500. That means the wealth environment behind this market has gotten considerably stronger, even as contract volume has stayed relatively quiet. A steady flow of new development inventory has been absorbing buyer activity, so it reflects a shift in the mix between resale and new construction more than an absence of demand.

This corridor has shown before that it can move fast. The recovery from near zero in early 2020 to 36 contracts by mid-2021 happened within a few quarters, and the current setup, with equity wealth at a decade high and contract volume still subdued, looks similar to conditions that preceded those earlier surges.

For buyers, the spread between broader market strength and local luxury volume represents one of the more compelling entry points across Manhattan submarkets right now. For sellers, understanding where this market sits in its cycle is important for positioning and pricing well as velocity continues to rebuild heading into 2026.

These charts plot $4M+ luxury contracts against the S&P 500 from 2016 through early 2026, overlaid with the average federal interest rates. It shows how luxury buyer demand has responded to shifting rate conditions, and where it stands relative to a decade of equity market growth.