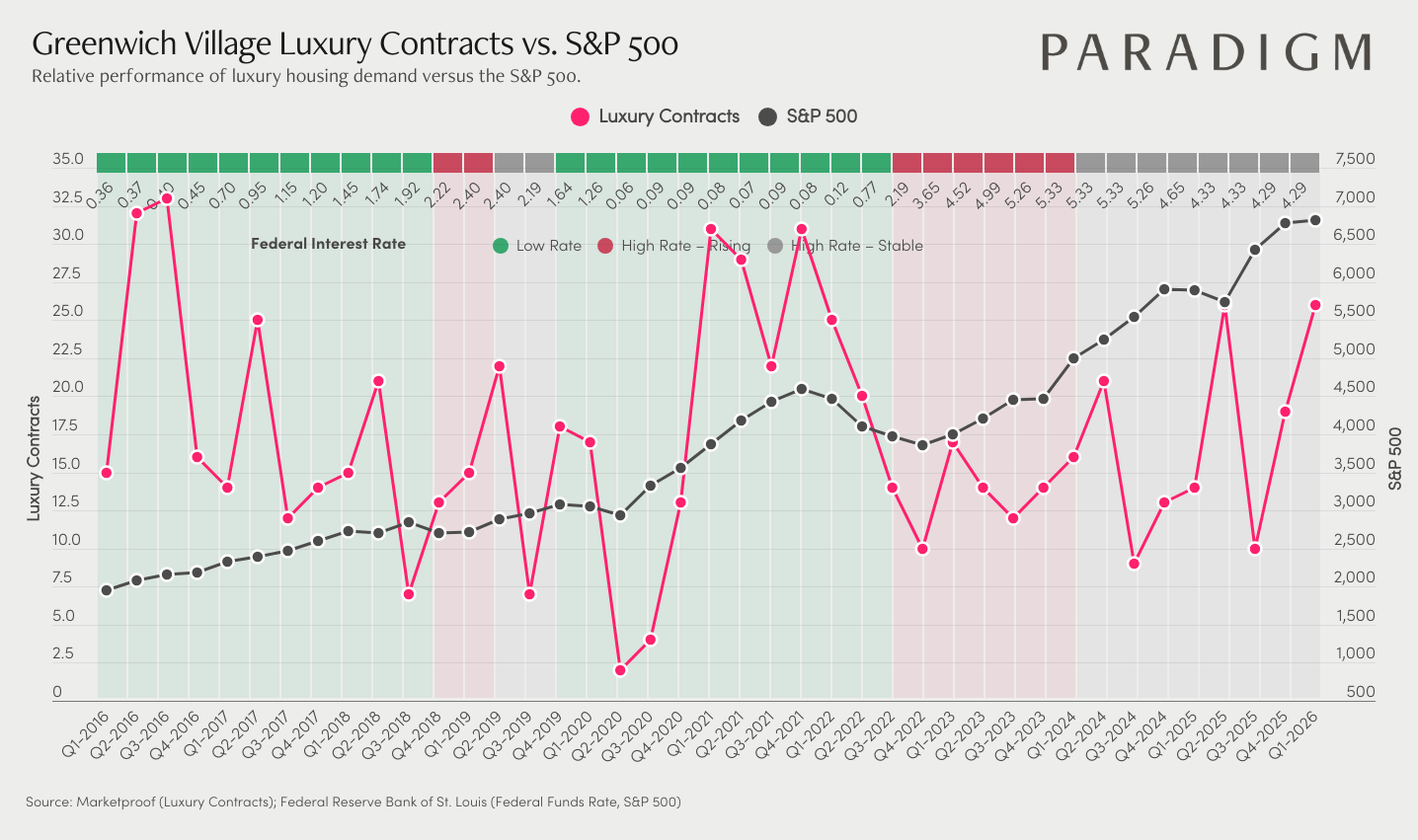

Greenwich Village has one of the strongest $4M+ contract track records in Manhattan. Volume hit 32 contracts in both Q2 and Q3 2016, stayed active through 2017 and 2018, and climbed back to around 21 in Q1 2021 during the post-COVID rebound. Very few corridors in the city have shown that level of sustained buyer conviction across multiple cycles.

Like the West Village, Greenwich Village is a market where limited inventory and high-value transactions mean a small number of deals can move quarterly volume significantly. Since 2022, contracts have ranged between 10 and 25, with periodic pushes toward the higher end of that range confirming that premium buyers are still stepping in when the right product comes along. That volatility is a feature of this market, not a weakness, and it means activity can accelerate quickly once momentum builds.

With the S&P climbing from around 4,000 to nearly 6,500 since 2022 while contract volume has stayed in a relatively narrow band, the gap between equity wealth creation and local luxury activity is one of the wider spreads this neighborhood has seen in the past decade. The wealth environment has been building while transaction volume has stayed selective, pointing to meaningful pent-up demand waiting for the right catalyst.

For buyers, Greenwich Village at current volume levels means access to one of Manhattan's most iconic neighborhoods with less competition than this market typically produces. For sellers, this neighborhood has historically moved in sharp bursts, and with contracts already nudging back toward 25 heading into Q1 2026, the advantage goes to those who are positioned ahead of the next acceleration with a lot of new developments coming.

These charts plot $4M+ luxury contracts against the S&P 500 from 2016 through early 2026, overlaid with the average federal interest rates. It shows how luxury buyer demand has responded to shifting rate conditions, and where it stands relative to a decade of equity market growth.