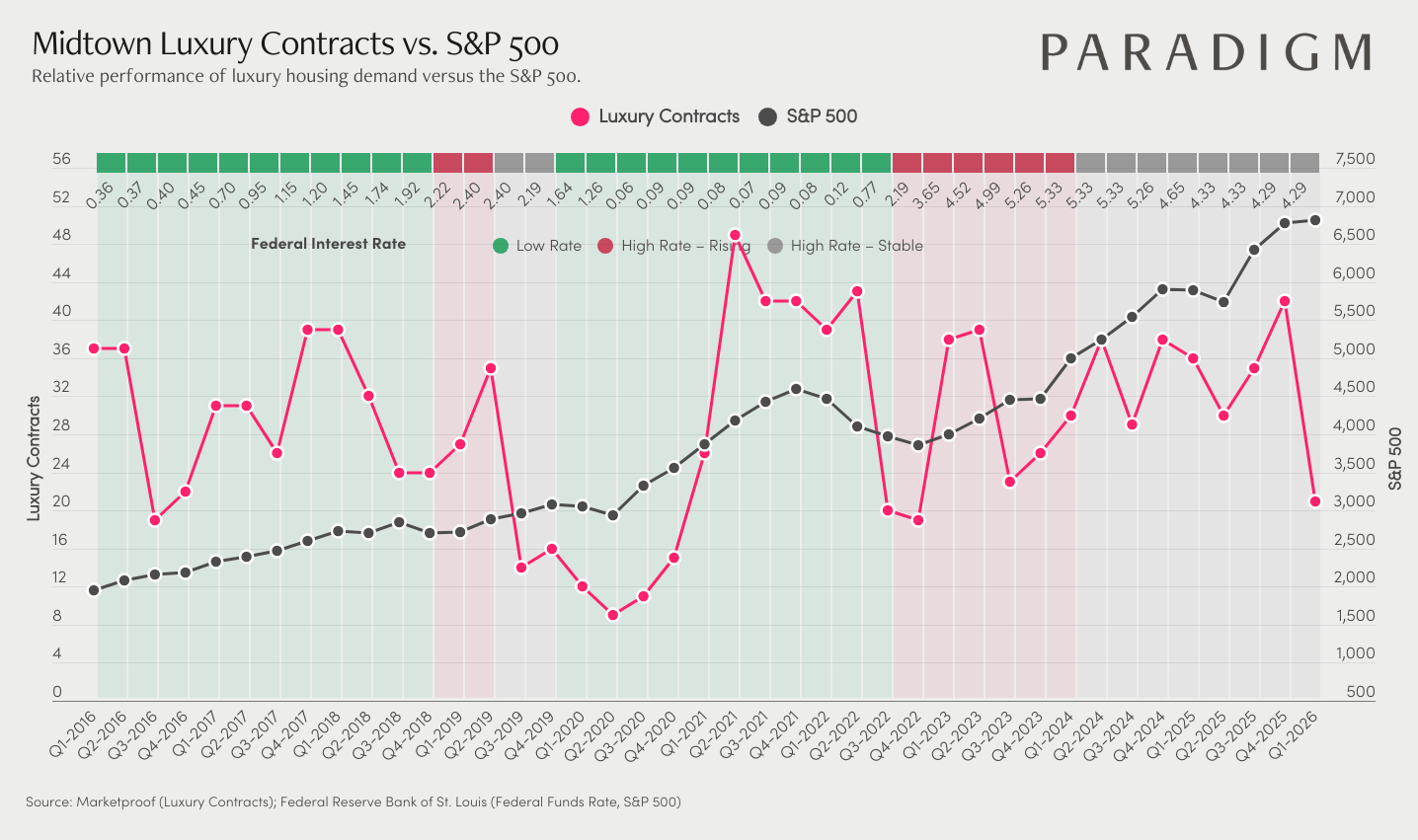

Midtown's $4M+ contract market has real scale and a consistent track record across multiple cycles. Volume started near 36 contracts in early 2016, held in the 30 to 39 range through much of 2018, and climbed back to 43 during the 2021 to 2022 rebound before pulling back as rates rose. Across different rate environments, Midtown has demonstrated a reliable ability to absorb luxury demand, but is oversupplied with inventory.

What makes Midtown distinct from other Manhattan submarkets is the depth of inventory. A significant amount of new development product has come to market over the past several years and is actively being absorbed. From a cycle perspective that is constructive: pricing is recalibrating, inventory is clearing, and the groundwork for the next period of stronger velocity is being laid. Midtown has done this before, and historically once absorption hits a tipping point the upside follows.

Contract volume has ranged between 19 and 38 over the past two years, and the gap between S&P 500 performance and local luxury activity is wider here than in most other Manhattan submarkets. The equity wealth environment has kept building while transaction volume has stayed measured, which points to a reservoir of demand that has not fully shown up yet. With the S&P near 6,500 and contracts around 20 heading into Q1 2026, that spread is difficult to ignore.

For buyers, Midtown is one of the more compelling value stories in Manhattan luxury right now: available inventory, competitive pricing relative to historical levels, and a strong wealth backdrop for those thinking longer term. For sellers, strategic pricing that aligns with current absorption trends is key, and the ongoing clearing of inventory is setting the stage for stronger velocity ahead.

These charts plot $4M+ luxury contracts against the S&P 500 from 2016 through early 2026, overlaid with the average federal interest rates. It shows how luxury buyer demand has responded to shifting rate conditions, and where it stands relative to a decade of equity market growth.