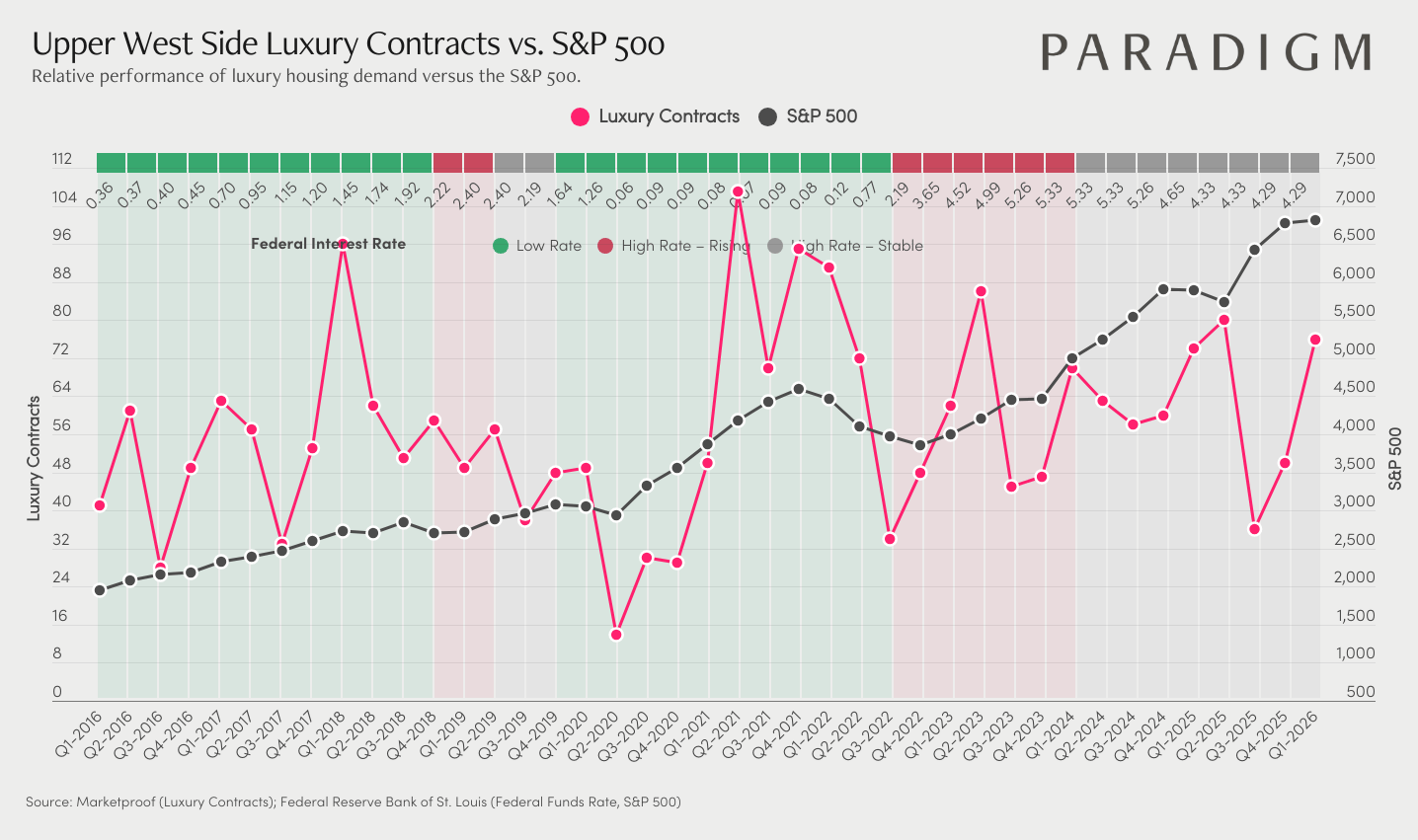

Since 2016, $4M+ luxury contracts on the Upper West Side have moved independently of the S&P 500, and the gap between the two has been especially pronounced in recent years. Contract volume peaked around 91 in Q2 2021 before pulling back sharply through 2022 and into 2023, bottoming near 33 contracts while the S&P continued climbing toward 4,500. That divergence reflects how rate-sensitive this market became once borrowing costs started rising.

What stands out is how the Upper West Side has historically snapped back. After the COVID low in early 2019, volume recovered quickly, and after the 2022 to 2023 trough, activity has been rebuilding steadily. By Q1 2026, contracts are back up to around 72, even as the S&P holds near 6,500, suggesting buyers have adjusted to the rate environment and are re-engaging on their own terms.

The Upper West Side tends to move in cycles of consolidation followed by sharper recoveries, and the current trajectory fits that pattern. For buyers, the spread between equity market strength and luxury contract volume still points to relative value that may not last as momentum builds. For sellers, the improving trend heading into 2026 is a good reason to feel confident about listing now, before that recovery fully prices in.

These charts plot $4M+ luxury contracts against the S&P 500 from 2016 through early 2026, overlaid with the average federal interest rates. It shows how luxury buyer demand has responded to shifting rate conditions, and where it stands relative to a decade of equity market growth.