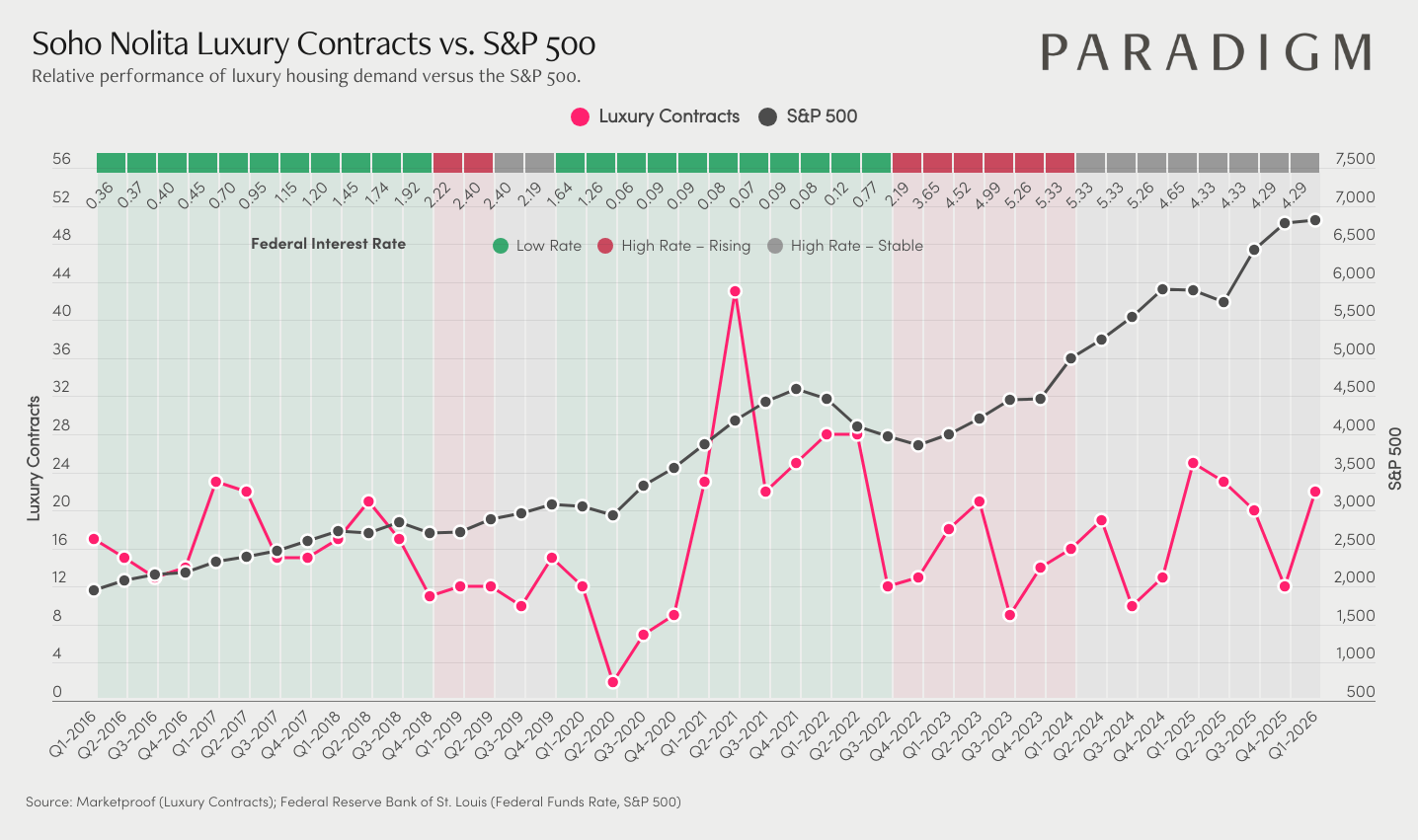

SoHo and Nolita have shown a consistent ability to generate sharp bursts of $4M+ contract activity, even in challenging rate environments. Volume hit 22 contracts in Q4 2016 and Q1 2017, then surged to 42 in Q1 2021, one of the strongest single-quarter readings across any submarket we track. When conditions align here, buyers move quickly.

That pattern has continued even through the high-rate period. Since 2022, contract volume has oscillated between 8 and 28, with recurring upward pulses showing an active buyer pool that steps in when the right product surfaces. The S&P meanwhile has climbed from around 4,000 to nearly 6,500 over the same stretch, widening the gap between equity wealth creation and local luxury activity considerably.

With volume currently around 21 contracts heading into Q1 2026 and the wealth environment at a decade high, SoHo and Nolita sit in a similar position to conditions that preceded earlier acceleration periods. This neighborhood has historically converted financial market strength into deal activity once buyer confidence catches up, and the current setup points in that direction.

For buyers, the present volume level offers one of the more favorable entry points this submarket has seen in recent years, particularly given how limited inventory remains. For sellers, the recurring activity pulses in the data confirm that well-priced listings are still finding buyers, and any shift in the rate environment could accelerate that meaningfully given the amount of wealth sitting on the sidelines.

These charts plot $4M+ luxury contracts against the S&P 500 from 2016 through early 2026, overlaid with the average federal interest rates. It shows how luxury buyer demand has responded to shifting rate conditions, and where it stands relative to a decade of equity market growth.