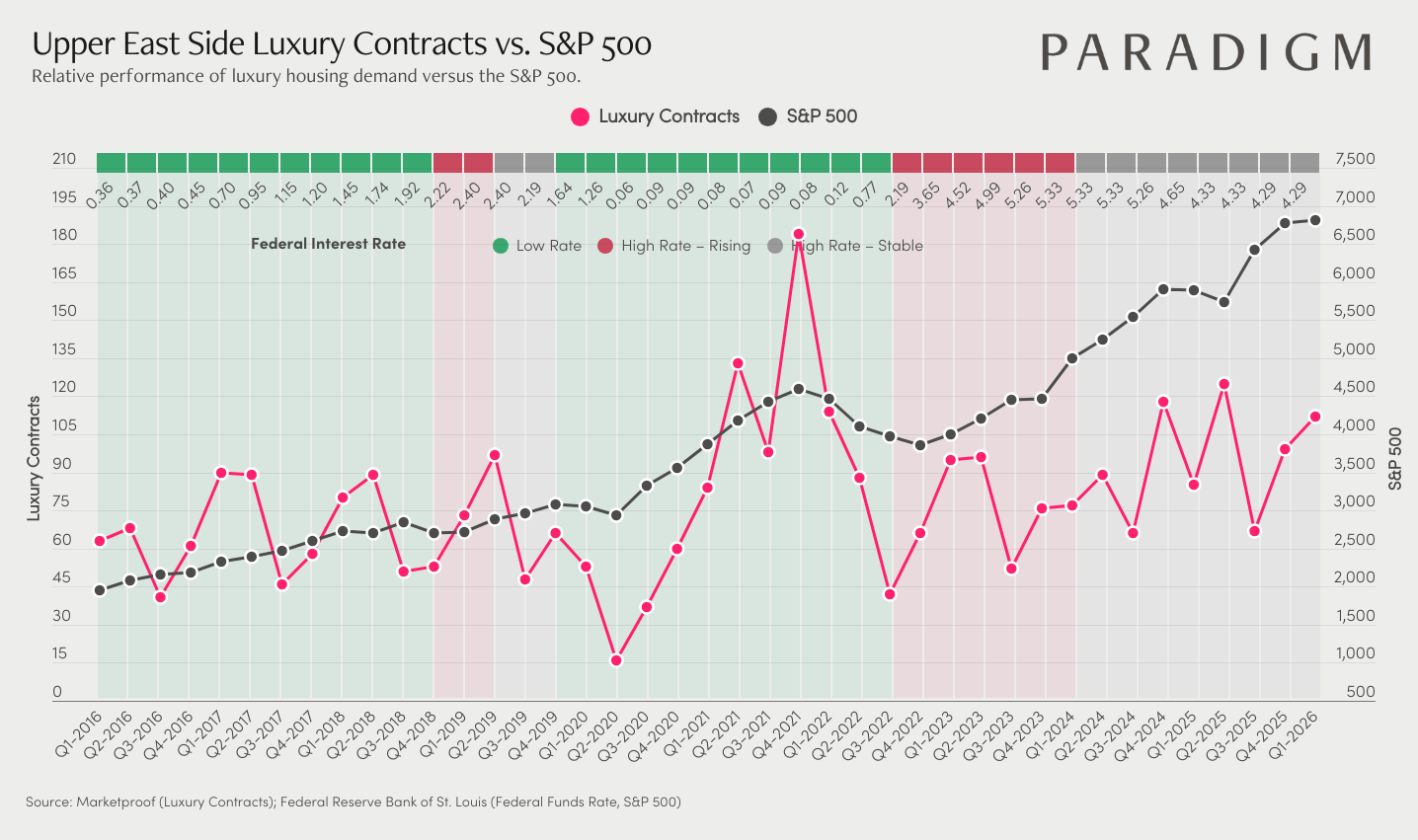

Since 2016, luxury contracts on the Upper East Side have consistently moved to their own beat, often diverging from the S&P 500. While the index climbed steadily from around 2,200 in early 2016 to nearly 6,500 by late 2024, $4M+ contract volume swung dramatically, peaking near 130 contracts in Q3 2021 before falling into the 45 to 75 range through much of 2023 and 2024. That divergence tells a clear story: luxury real estate demand here is not simply a function of equity wealth. It runs on its own fundamentals, things like inventory, buyer sentiment, and neighborhood-level demand.

What makes the rate environment particularly telling is how contract volume behaved once rates stabilized. After the sharp pullback during the high-rate rising period, volume began recovering even while rates held in the 4.29 to 5.33 range through 2024 and into 2026. Buyers adjusted. The paralysis of the rising-rate shock faded, and activity started rebuilding on its own terms.

Heading into Q1 2026, with contracts back up to around 108 and the S&P holding near 6,700, the gap between equity wealth creation and luxury contract volume is narrowing again. For buyers, that convergence points to a window where pricing has not fully caught up to the wealth environment around it. For sellers, the improving velocity signals that demand is rebuilding, and being well positioned now means you can catch that momentum as the recovery continues.

These charts plot $4M+ luxury contracts against the S&P 500 from 2016 through early 2026, overlaid with the average federal interest rates. It shows how luxury buyer demand has responded to shifting rate conditions, and where it stands relative to a decade of equity market growth.